With more consumers paying $1,000 or more monthly for their car loans, it is no surprise we are seeing growing loan defaults.

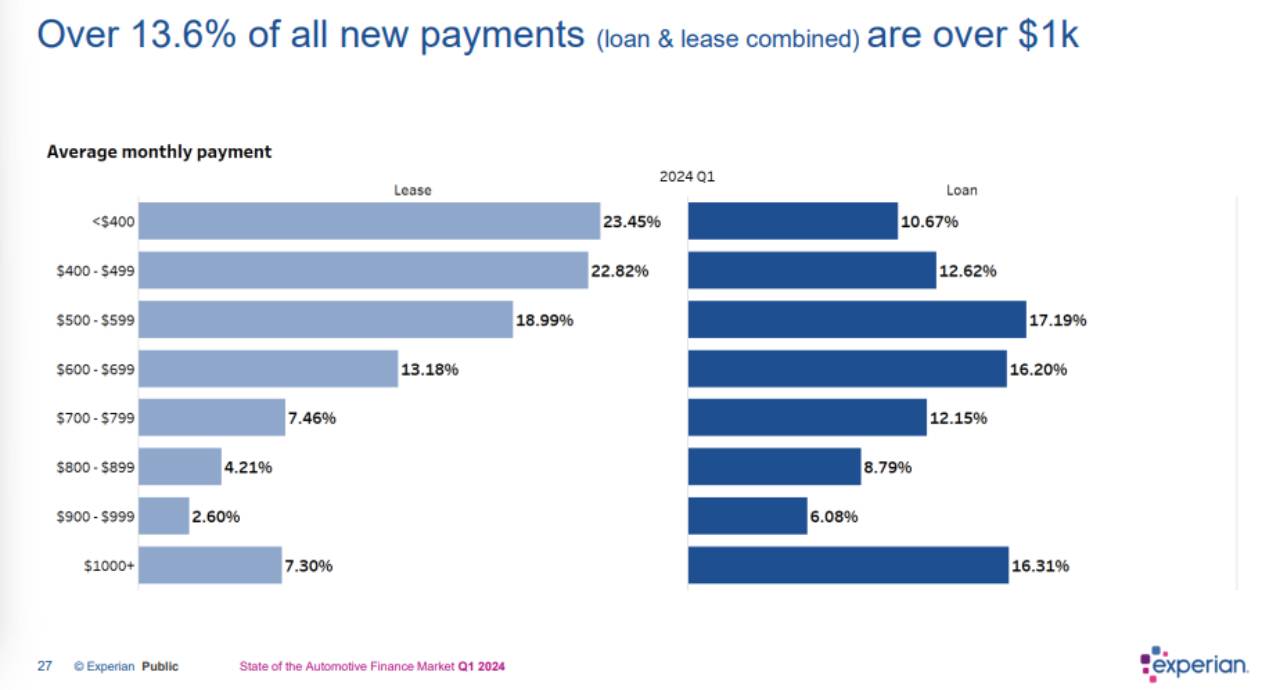

Car payments are reaching numbers that look more like mortgage payments. According to Experian, in Q1 of 2024, 16.31% of all new monthly car loans were $1,000 or more.

For the same period, leases over $1,000 per month were 7.3%.

Used car buyers aren’t immune either, with 4.63% of consumers paying over $1,000 monthly.

The average new car payment was $735 per month in the first quarter of 2024, a .04% increase from the same period in 2023.

According to Experian, the average new car loan in Q1 of 2024 was $40,634, and the average used vehicle loan was $26,073. Both numbers reflect a slight increase from Q4 in 2023.

Reasons for the large payments

There are several factors contributing to this issue including the pandemic, interest rates, and shorter auto loan terms.

1. Pandemic

The pandemic brought a surge in car buying but a decrease in manufacturing, which increased prices for new and used cars. During this period, auto loan balances skyrocketed.

In 2021, I sold my 2018 Ford Fusion SE to Carvana for top dollar. Although it had extremely low miles, it was still a four-year-old car. Carvana offered me $15,600 for it. A few weeks later, I saw them list it for $25,600. I paid $29,000 for it in 2018. Car manufacturers also added “market adjustments” because they knew they could.

Essentially, car buying for many years was a seller’s market, putting consumers in a difficult position.

2. Auto Loan Rates

Fast-forwarding and auto loan rates are higher than they have been in decades. According to Nerdwallet, for consumers with good credit, auto loans currently average 7% for new and 9% for used as of June 27, 2024.

3. Length of Loan

Finally, some people are taking shorter loan terms to obtain better financing terms. Since the length of an auto loan can impact rates, many are choosing shorter terms like two or three years. This saves on total interest for the life of the loan.

Auto loan defaults are increasing

These high payments are starting to cause financial strain. As car values decline, some buyers may owe more than their car is worth, and many are beginning to default on their payments.

In Q1 of 2024, 2.71% of auto loans were at least 30 days late. Auto loans that were 30 days past due for the same period last year were 2.23%.

While these are not all time highs, the trends are moving upward.

“Delinquency transition rates have pushed past pre-pandemic levels, and the worsening appears to be broad-based,” researchers at the New York Fed wrote in a blog post. “Loans opened during 2022 and 2023 are, so far, performing worse than loans opened in earlier years, perhaps because buyers during these years faced higher car prices and may have been pressed to borrow more, and at higher interest rates.”

Ways to get a better auto loan rate

If you are in the market for a new car, the following are some ways you can reduce your loan rate.

- Check your credit score. Auto lenders will determine your rate based on your credit. Prime, sub-prime and other categories all have varying rates. Make sure your credit report does not reflect delinquencies or defaults before car shopping.

- Larger down payment. The more you can put down, the less y our loan will be seen as a risk. This can result in lower interest rates.

- Have a cosigner. If you are a first-time car buyer, or have credit issues, a co-signer with good credit can help you get a lower rate.

- Shop around. There is no requirement to use a dealers lender. Check with your bank, credit union, or online lender to see if they can offer better rates.

- Set realistic expectations. You might want that Mercedes, but if your income does not justify it, be honest with yourself. Cars depreciate the minute they leave the lot, it makes more sense to put that money into something that can make you more money.